The future of the child tax credit hangs in the balance as the Biden administration pushes through the Build Back Better bill, which would extend the benefit through 2022. (iStock)

Expanded Child Tax Credit (CTC) payments have been a lifeline for many American families during the coronavirus pandemic. According to Census Bureau Data.

The Build Back Better Act would extend this benefit through 2022 and make credit permanently available to low-income families. But as President Joe Biden’s social spending bill lingers in Congress, the future of CTC payments is unknown.

Keep reading to learn more about how Americans are using the Child Tax Credit and your alternative debt repayment options if the CTC isn’t extended. You can visit Credible to compare interest rates on debt consolidation loans for free without affecting your credit score.

HOW YOUR TAX FILE CAN IMPROVE YOUR CREDIT

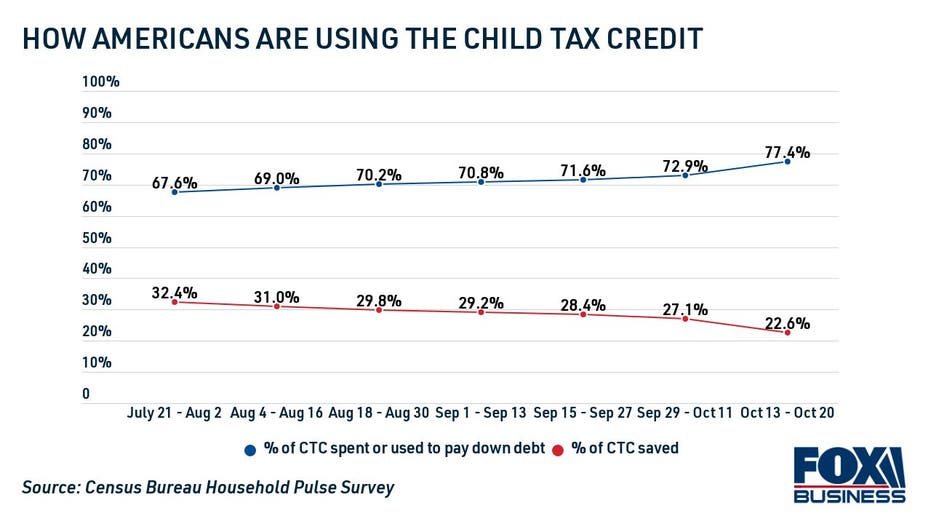

More households use their child tax credit than they save

The American rescue plan, which was signed into law by President Biden in March 2021, increased the amount of the child tax credit and automatically distributed the credit in monthly installments ranging from $250 to $300 per eligible child. Millions of American families qualify for the full amount, with income caps of $150,000 for married couples and $112,500 for single-parent households.

When families started receiving advance payments in July, about two-thirds (68%) of them used the CTC payment to top up expenses or pay off debts, while one-third (32%) were able to save money, according to the Census Bureau Household Pulse Survey. Over time, fewer families were able to save the credit – less than 1 in 4 recipients (23%) were able to save money, while the vast majority (77%) spent the CTC payment.

5 REASONS TAXPAYERS TO FILE TAXES EARLY

Low-income families are even more dependent on expanded credit. Recent research from the Center on Budget and Policy Priorities (CBPP) found that 91% of households with incomes below $35,000 rely on CTC payments to cover basic expenses, such as food, shelter and education. The CBPP also found that making the expanded CTC permanent would reduce child poverty by more than 40%.

However, the final CTC payment was distributed in December and it will not continue into 2022 unless lawmakers come together to pass the Build Back Better Act. The $1.7 trillion spending bill needs the support of all Democrats in the Senate to pass without Republican support, but was stalled beyond its original Christmas deadline when the moderate senator Joe Manchin of West Virginia supported the legislation.

If you were relying on the child tax credit to pay off your debt, you may need to look for other methods of paying off debt in the new year as the future of CTC payments is not not clear. You can learn more about paying off your debt by contacting a knowledgeable loan officer at Credible.

MILLIONS WILL NOT BENEFIT FROM FULL PAYMENT FOR COVID-19 ECONOMIC IMPACT

How to Pay Off Debt Without CTC Payments

High-interest debt is a heavy financial burden that can make it difficult for families to pay for other necessary expenses like childcare, rent, and utilities. If you’re struggling to pay off your debt without the Child Tax Credit, consider some alternative debt repayment strategies:

- Non-profit credit counseling. A credit counselor can analyze your finances to help you create a budget through free financial education. They may also enroll you in a debt management plan (DMP) to pay off what you owe, and they may be able to negotiate with your creditors to settle the debt for less than you owe or reduce your interest rate. Some credit counseling agency services can be inexpensive.

- Debt consolidation loans. This is a type of unsecured lump-sum personal loan that is used to pay off high-interest debt like credit card balances and payday loans. You will pay off your debt in fixed monthly installments over a set period of time, usually a few years. Personal loan interest rates are currently near their lowest levels, but the rate you qualify for depends on your credit score and debt-to-equity ratio, among other eligibility criteria.

- Balance transfer cards. Borrowers with very good credit may be eligible to transfer multiple credit card balances to a new card at a lower interest rate. Some credit card issuers are offering 0% APR introductory offers for creditworthy borrowers who open a balance transfer credit card. Keep in mind that some issuers charge a balance transfer fee of 3-5% of the total amount transferred. You can compare balance transfer offers on Credible for free.

If you decide to borrow a debt consolidation loan, it is important to compare the offers of several lenders to find the lowest possible rate for your financial situation. You can see the estimated interest rates for your debt consolidation loan for free without affecting your credit score on Credible, so you can determine if this method of debt repayment is right for you.

BUILD BACK BETTER PLAN WILL REDUCE THE COST OF INSTALLING SOLAR PANELS BY 30%, SAYS THE WHITE HOUSE

Do you have a financial question, but you don’t know who to contact? Email the Credible Money Expert at [email protected] and your question might be answered by Credible in our Money Expert column.